Read this glossary term guide to understand the legal definition of collateral, how it works in borrowing and debt, and what assets can and cannot be used as collateral. Plus, explore different types of collateralized debt obligations and more!

What is Collateral?

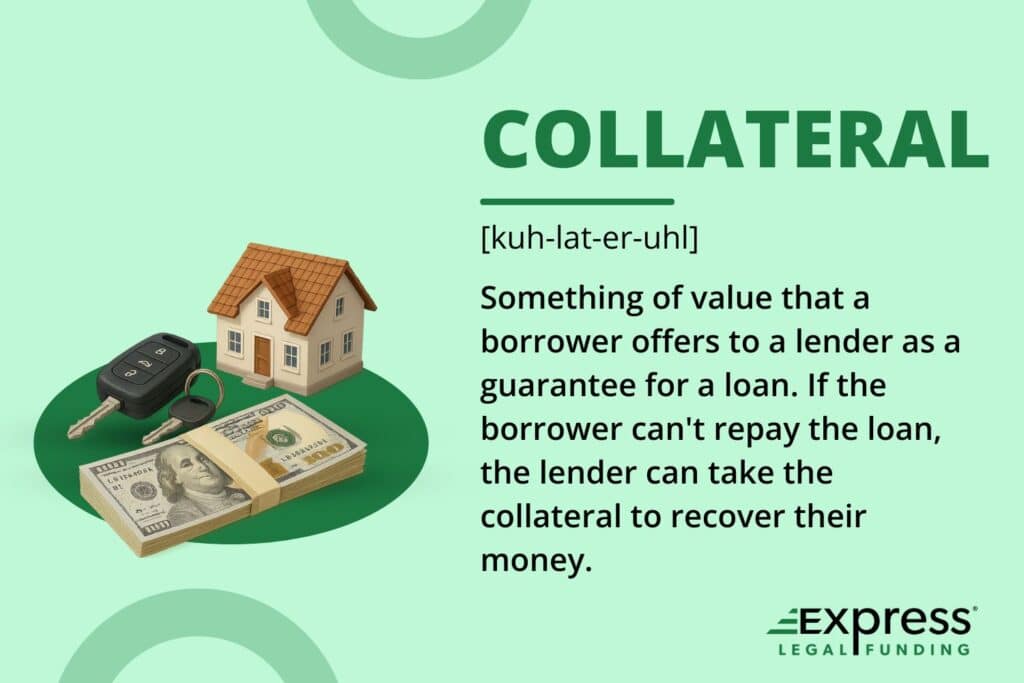

Collateral is an asset that a borrower pledges to a lender as security for a loan. It serves as protection for the lender, ensuring that if the borrower fails to repay, the lender has the right to seize and sell the asset to recover the outstanding debt.

Common examples of collateral include homes (for mortgages), vehicles (for car loans), and financial assets like stocks or bonds. The presence of collateral often helps borrowers secure better loan terms and lower interest rates.

What are Collaterals?

Collaterals generally refer to assets or property that a borrower pledges to a lender as security for a loan or credit. When someone takes out a loan, the lender may require collateral as a form of guarantee that they will be able to recover their money in case the borrower fails to repay the loan. Collateral acts as a backup source of payment for the lender.

Common types of collateral include real estate, vehicles, financial investments, valuable possessions, or future income streams.

If the borrower defaults on the loan or cannot repay it according to the agreed terms, the lender has the right to seize and sell the collateral to recover the outstanding debt.

Collateral provides the lender with a level of security and reduces the risk associated with lending money.

What can be used as Collateral for a Loan?

Various types of assets can be used as collateral for a loan, depending on the lender’s requirements and the nature of the loan. Some common examples include the following:

- Real Estate: residential or commercial properties, including houses, apartments, land, or buildings, can serve as collateral for loans. The lender may conduct an appraisal to determine the value of the property.

- Vehicles: Cars, trucks, motorcycles, boats, or other vehicles can be used as collateral. The lender may assess the vehicle’s condition, model, and market value to determine its suitability as collateral.

- Financial Assets: Investments such as stocks, bonds, mutual funds, or certificates of deposit (CDs) can be pledged as collateral. The lender may require documentation to verify the ownership and value of these assets.

- Savings or Deposits: Some lenders allow borrowers to use their savings accounts, fixed deposits, or other cash reserves as collateral, essentially freezing the funds until the loan is repaid. For some types of loans, the lender can take automatic payments electronically by withdrawing the owed funds from the borrower’s bank account as repayment.

The borrower would have previously given ACH authorization to the lender, which may be a loan contract term. It’s important to note there are instances where it is illegal for lenders to take automatic electronic payments, such as active duty military members and their families under the MLA. - Valuables: High-value possessions like jewelry, artwork, collectibles, or antiques may be accepted as collateral. The lender may require appraisals or expert assessments to determine their value. For smaller pawn shop loans, the owner or an employee typically appraises the pawned item (an asset used as collateral at pawn shops) and does not hire a third-party appraiser.

- Future Income: In certain cases, future income streams can be used as collateral. This applies to loans based on anticipated future earnings, such as personal loans for self-employed individuals or small business owners.

What are the Types of Collateral?

There are several types of collateral that are classified based on their nature and characteristics. Here are some common types of collateral:

- Real Estate Collateral: This includes residential properties, commercial properties, and land. Real estate collateral is often considered valuable due to its tangible and relatively stable nature.

- Vehicle Collateral: Vehicles such as cars, trucks, motorcycles, boats, or recreational vehicles can be used as collateral. The resale value of the vehicle is assessed to determine its eligibility as collateral.

- Financial Collateral: This refers to financial assets that can be pledged as collateral, including stocks, bonds, mutual funds, certificates of deposit (CDs), or other investment instruments. The value of the financial asset is considered when determining its suitability as collateral.

- Cash Collateral: Cash or cash equivalents, such as savings accounts, fixed deposits, or money market accounts, can be used as collateral. The lender typically holds the funds as security during the loan term.

- Equipment and Inventory Collateral: Business loans or lines of credit may involve using equipment, machinery, or inventory as collateral. This is common in industries where specific assets, such as manufacturing, construction, or retail, play a crucial role.

- Receivables Collateral: Accounts receivable or outstanding invoices owed to a business can be used as collateral, particularly in asset-based lending. The lender may take control of the receivables or require a lien on them.

- Valuables Collateral: High-value possessions like jewelry, artwork, antiques, or collectibles can serve as collateral. Lenders typically require an appraisal service to determine how much jewelry or artwork is worth.

- IP Assets: Assets that lack physical forms, such as intellectual property, copyrights, trademarks, or patents, can be accepted as collateral for loans based on the liquidated value of a company’s IP assets. Intellectual property assets can be challenging to place a value on and sell in case of default.

What cannot be used as Collateral for a Loan?

While many types of assets can be used as collateral for a loan, certain assets are typically not accepted as collateral by lenders. The following list includes types of assets that can’t be used as collateral:

- Personal Items of Minimal Value: Everyday personal items like clothing, furniture, electronics, or appliances are generally not considered suitable collateral due to their relatively low value and limited marketability.

- Consumable Goods: Items with a limited shelf life, such as food, beverages, or perishable goods, are not generally accepted as collateral because they cannot retain their value or serve as long-term assets.

- Non-Transferable Assets: Assets that are legally restricted from being transferred, such as government benefits, social security payments, or certain insurance policies, cannot be used as collateral since they cannot be seized or sold.\

- Illegal or Prohibited Assets: Assets acquired or used unlawfully, such as illicit drugs or contraband items, cannot be used as collateral due to their illegal nature.

- Stolen Property: Stolen assets that the borrower does not own cannot be put up as collateral. Using stolen property as collateral is fraud. For example, the borrower uses someone else’s home title to qualify for a mortgage.

- Future Potential Income: While future income can sometimes be used as collateral in specific circumstances, traditional lenders typically do not accept it as collateral for standard loans. Future income is uncertain and cannot be easily quantified or controlled by the lender.

What is a Collateralized Debt Obligation?

A collateralized debt obligation (CDO) is a complex financial instrument that pools together a portfolio of various debt assets, such as bonds, loans, and other fixed-income instruments. These assets are then divided into different tranches or layers, each with different levels of risk and return.

CDOs are structured products that are typically issued by special-purpose vehicles (SPVs) or entities created specifically for this purpose.

The SPV purchases a diverse range of debt securities, including mortgage-backed securities (MBS), asset-backed securities (ABS), corporate bonds, and bank loans.

These debt securities serve as the collateral for the CDO. The CDO’s cash flows are derived from the interest and principal payments made on the underlying debt assets.

The cash flows are then distributed to the CDO investors based on the priority of their tranche. The tranches are usually classified as senior, mezzanine, and equity, with senior tranches prioritizing cash flow for investors but offering lower returns.

In comparison, equity tranches have a lower priority but offer potentially higher returns. CDOs became particularly prominent in the early 2000s, with the rise of mortgage-backed securities (MBS) and the securitization of subprime mortgages.

However, they gained notoriety among the general public during the global financial crisis of 2008 when the underlying subprime mortgage assets experienced a significant percentage of defaults, leading to substantial losses for investors and contributing to the overall market turmoil.

MBS and CDO containing junk mortgages are two investment instruments that led to the bankruptcy and subsequent end of Lehman Brothers during the 2008 global financial crisis.

What is the Difference Between a Lien and Collateral?

A lien and collateral are related concepts, but have distinct meanings and implications in the context of loans and financing. There are differences between the two.

Collateral refers to an asset or property that a borrower pledges to a lender as security for a loan or credit. It serves as a form of protection for the lender in case the borrower defaults on the loan.

The collateral can be seized and sold by the lender to recover the outstanding debt. Collateral acts as a risk mitigation mechanism for the lender and provides a tangible asset that can be liquidated to cover losses.

On the other hand, a lien is a legal claim or encumbrance placed on a property or asset to secure the payment of a debt. The creditor has the right to satisfy the debt by accessing the property or asset.

A lien can be established through a legal agreement or by operation of law. It provides the creditor with a legal interest or right over the asset, which can be enforced if the debtor fails to meet their obligations.

The key difference between the two is that collateral is the actual asset or property pledged by the borrower to secure a loan, while a lien is a legally allowed claim or interest that the creditor holds over the collateral, giving them the right to enforce the claim if the borrower defaults on the loan.

What Happens if You Sell Collateral?

If you sell the collateral on a loan, you still owe money, you could be in breach of contract, and the lender will demand repayment in full immediately. However, depending on your repayment status, a lender can sell the collateral.

When a lender sells collateral that a borrower had pledged, it typically occurs because the borrower has defaulted on the loan. Defaulting on a loan means failing to meet the repayment obligations per the signed loan contract.

The specific process and outcomes can vary based on the jurisdiction, the terms of the loan agreement, and applicable laws. Here’s a general overview of what happens when collateral is sold:

- Default and Notification: When a borrower defaults on a loan, the lender will typically provide a formal notice to the borrower regarding the default and their intent to sell the collateral. The notice period allows the borrower an opportunity to rectify the default or make alternative arrangements.

- Seizure and Evaluation: The lender may seize the collateral if the default is not resolved. The collateral is then evaluated to determine its fair market value. An appraisal or assessment may be conducted to determine the appropriate selling price of the property that is to be sold.

- Sale Process: The lender will initiate the sale process to liquidate the collateral and recover the outstanding debt. The sale can take various forms, such as a private sale, auction, or public sale, depending on the nature of the collateral and applicable laws.

- Application of Proceeds: Once the collateral is sold, the lender will use the proceeds to recover the outstanding debt. The proceeds are first applied to cover the principal amount owed and any accrued interest and fees.

If there are any remaining funds after satisfying the debt, they may be returned to the borrower. However, if the proceeds fall short of the total debt, the borrower may still be responsible for the remaining balance. - Deficiency or Surplus: If the proceeds from the sale of collateral are insufficient to cover the entire debt, the borrower may still be liable for the remaining amount, known as a deficiency. On the other hand, if the proceeds exceed the outstanding debt, the borrower may be entitled to the surplus amount.

Can an IRA be Used as Collateral for a Loan?

No, the IRS prohibits Individual Retirement Accounts (IRAs) from being used as collateral for a loan. The Internal Revenue Service (IRS) imposes strict rules and regulations on IRAs to maintain their tax advantages and deferred tax status, and using an IRA as collateral would violate these rules.

The purpose of an IRA is to provide individuals with a vehicle for saving and investing for retirement, and the funds in an IRA are meant to be preserved for retirement income.

Using an IRA as collateral could potentially jeopardize the tax benefits associated with the account.

However, it’s important to note that certain exceptions and provisions allow for temporarily withdrawing a portion of your IRA, which has a similar effect as if you could borrow against an IRA that does not trigger adverse tax consequences.

These include specific types of IRA loans, such as “60-day IRA rollover loans”, where the funds are temporarily withdrawn and repaid within a specific time frame, with a possible 12-month extension.

It’s crucial to consult with a financial advisor or tax professional who can provide guidance specific to your situation and help you understand the potential implications and available options for accessing funds or obtaining a loan while preserving the tax advantages of your IRA.