Because pre-settlement funding is regulated at the state level, many people ask who actually sets the rules. The video below explains how state laws, federal law, and courts each play a role.

The FAQs below explain how state and federal rules apply to pre-settlement funding (sometimes referred to as “lawsuit loans”), why some states limit certain funding agreements, and how to check whether funding is available for your case.

Is pre-settlement funding regulated under federal law?

No. There is no single federal law that directly regulates pre-settlement funding. Instead, regulation is handled at the state level through statutes, court decisions, and consumer protection rules. Because of this, legality, requirements, and availability can vary widely depending on the plaintiff’s state of residence or where a case is filed.

Legality of Pre-Settlement Funding by State

Why is pre-settlement funding illegal in some states?

Some states restrict pre-settlement funding to prevent high costs or unfair terms, or because they treat certain agreements as loans under lending laws. Others rely on older doctrines like champerty and maintenance, and some courts have found certain contracts unenforceable. That’s why rules vary by state, and funding may be limited or unavailable in some places.

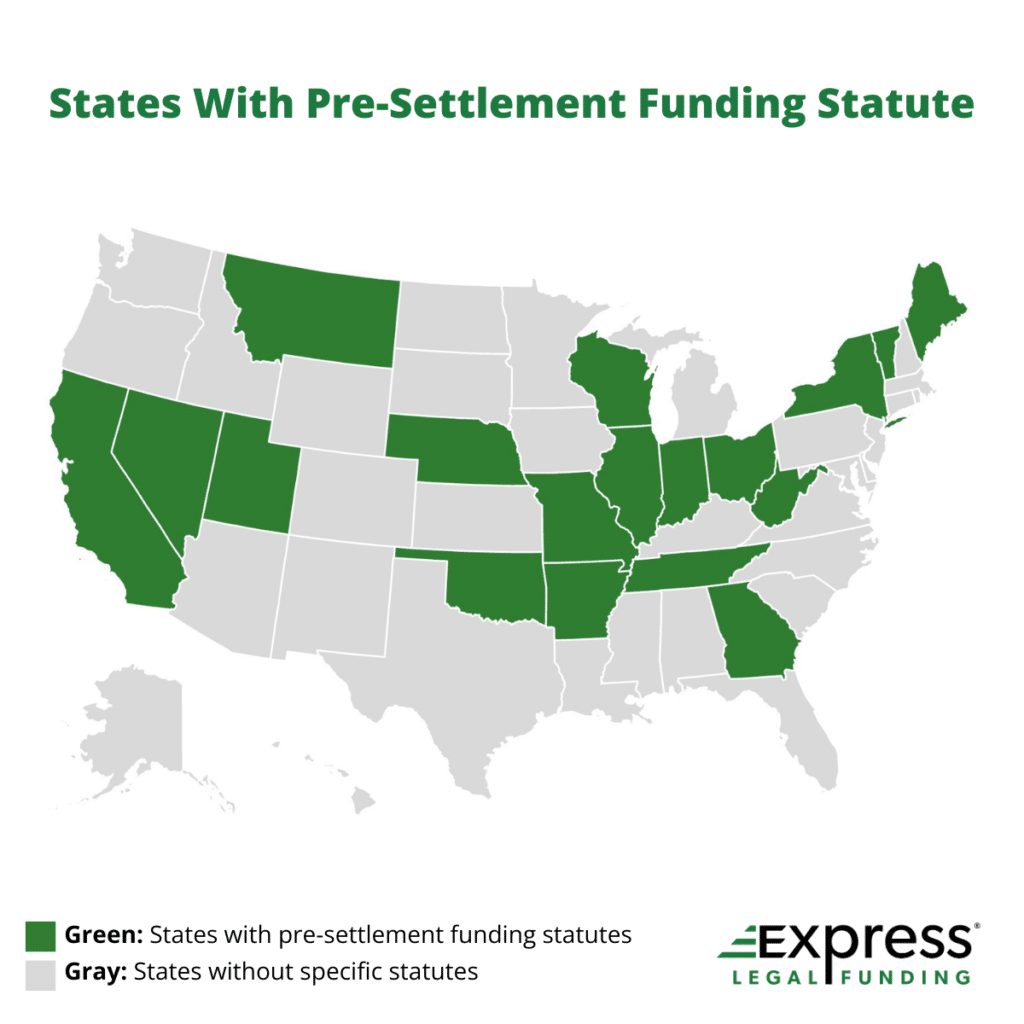

What states have laws regulating pre-settlement funding?

Several states have enacted laws that regulate pre-settlement funding agreements, often called consumer legal funding statutes. These regulations may require specific disclosures, impose rate or fee limits, or provide cancellation periods.

States with Pre-Settlement Funding Laws

The states with laws regulating pre-settlement funding include:

- Arkansas

- California

- Georgia

- Illinois

- Indiana

- Maine

- Missouri

- Montana

- Nebraska

- Nevada

- New York

- Ohio

- Oklahoma

- Tennessee

- Utah

- Vermont

- West Virginia

- Wisconsin

Although Arkansas and West Virginia have statutes addressing legal funding, their requirements and rate caps are highly restrictive, making pre-settlement funding unavailable or impractical for many providers in practice.

Regulatory requirements vary by state and may also classify certain agreements under existing consumer or lending laws.

Which states restrict or limit pre-settlement funding?

It depends on the contract structure and how each state’s laws are interpreted. The states that restrict or prohibit pre-settlement funding arrangements include Arkansas, Colorado, Kentucky, Maryland, North Carolina, and West Virginia. Because laws and court interpretations can change, it’s important to confirm current eligibility with your attorney.

Which states do not have consumer legal funding laws but treat pre-settlement funding as not a loan?

Some states do not have a consumer legal funding statute, but courts have held that non-recourse pre-settlement funding is not a loan because repayment is contingent on the outcome of the case. As a result, consumer lending laws may not apply in the same way they do to standard loans. These states include:

- Florida

- Michigan

- Minnesota

- Texas

Even in these states, pre-settlement funding agreements remain subject to contract law and court-enforceability standards. Laws and legal interpretations can change, so it’s important to confirm with your attorney how state rules apply to your specific pre-settlement funding agreement.

How am I protected if my state doesn’t have specific pre-settlement funding laws?

If your state doesn’t have a specific legal funding law, protections can still come from contract law, court oversight, and attorney involvement.

In addition, reputable providers often follow best practices promoted by organizations such as the American Legal Finance Association (ALFA), the Alliance for Responsible Consumer Legal Funding (ARC), and Legal Funders for Actually Fair Funding (LFAFF), which emphasize transparency, fairness, and ethical standards.

How can I check if pre-settlement funding is legal in my state?

Start by asking your attorney, since state rules can come from statutes and court decisions. Next, ask the funding company what state-specific requirements apply and request written disclosures and payoff examples. If the company can’t clearly explain legality, licensing (if applicable), or contract terms, treat that as a red flag.

Do pre-settlement funding laws change over time?

Yes. States can pass or update laws, regulators can issue guidance, and courts can change how they interpret legal funding agreements. That’s why older articles may be outdated and why it’s smart to confirm current rules in your state before relying on any single source. When in doubt, ask your attorney to verify.

What Pre-Settlement Funding Is and How It Works

Definition: What Is Pre-Settlement Funding?

Pre-settlement funding is a form of financial assistance available to plaintiffs who are waiting for a lawsuit to resolve. It provides a cash advance based on the expected value of a settlement or judgment, allowing plaintiffs to cover living expenses while their case is pending. Repayment usually comes from the case proceeds if the plaintiff wins or settles.

Non-Recourse vs. a Traditional Loan

Pre-settlement funding is typically non-recourse, meaning repayment depends entirely on the outcome of the case. If the plaintiff loses and recovers nothing, they usually do not have to repay the advance. This structure is different from a traditional loan, which requires repayment regardless of outcome and is governed by standard lending laws.

Relevant read: What Is Non-Recourse Legal Funding?

Why Some States Classify It as Lending

Some states treat certain pre-settlement funding agreements as loans, especially when they resemble traditional credit products, such as those requiring credit checks or include features like fixed repayment obligations. When courts or lawmakers view funding as lending, consumer lending laws—such as interest rate caps or licensing requirements—may apply. This classification can significantly affect how funding is offered in those states.

Relevant read: Does Pre-Settlement Funding Require Monthly Payments?

How State Law Affects Borrowers

Is pre-settlement funding considered a loan?

No. Pre-settlement funding is usually not a traditional loan. It is a non-recourse cash advance based on your expected settlement. You repay it only if you win or settle your case. If you lose, you typically owe nothing. Because repayment depends on the case outcome, some courts say consumer lending laws may not apply the same way they do to standard loans.

How does state law affect the cost of pre-settlement funding?

State law can significantly affect cost. In states with consumer legal funding regulations, laws may require disclosures, limit fees, or impose rate caps. In states with fewer rules, pricing is more market-driven. That’s why costs can vary by state and provider, making it important to review payoff examples and contract terms carefully.

Relevant read: How Much Does Pre-Settlement Legal Funding Cost?

Can I get pre-settlement funding if my state restricts it?

Sometimes. A state restriction does not always mean funding is impossible. Availability often depends on how the contract is structured, applicable court rulings, and whether the funding complies with state law. In restricted states, attorney involvement is especially important to determine whether a legal funding agreement is permitted for your case.

Attorney Involvement and Lawsuit Impact

Do I need my attorney’s approval to get pre-settlement funding?

In most cases, yes—even if your state’s law doesn’t explicitly require it. Reputable pre-settlement funding companies typically need your attorney’s cooperation to verify case details and coordinate repayment from settlement proceeds. Attorney involvement also helps ensure the agreement is accurate, ethical, and does not interfere with your legal strategy or settlement decisions.

Relevant read: Do I Need a Lawyer to Get Legal Funding?

Does pre-settlement funding affect my lawsuit or settlement?

No. Pre-settlement funding should not affect how your lawsuit is handled, aside from providing temporary financial relief while your case is pending. Reputable legal funding companies cannot control your case, your attorney, or settlement decisions—and some state laws explicitly prohibit funders from influencing litigation.

Because funding costs can increase over time, it’s important to borrow only what you need and understand how repayment grows if your case takes longer than expected.

What happens if I lose my case?

If your funding agreement is non-recourse, you typically do not repay anything if you lose your case and recover no settlement or judgment. This is a key difference between pre-settlement funding and traditional loans. Always confirm that non-recourse terms are clearly stated in your agreement before accepting funding.

Conclusion: How to Verify Eligibility and Find Safe, Legal Funding

Summary of legality

Pre-settlement funding is legal in most U.S. states, but not all. Because there is no single federal law governing legal funding, each state sets its own rules through statutes, court decisions, and consumer protection standards. That’s why eligibility and availability depend on where your case is filed and how the funding agreement is structured.

Final advice

Before you move forward, involve your attorney and confirm what rules apply in your state. Review written disclosures, request payoff examples, and make sure the agreement is truly non-recourse. If a funding company can’t clearly explain its terms, costs, and compliance approach, treat that as a red flag.

Apply with Express Legal Funding to Get Pre-Settlement Funding

If you need financial support while your case is pending, Express Legal Funding offers transparent, non-recourse pre-settlement funding with attorney coordination and clear payoff disclosures. You can apply online or call us at (888) 232-9223 to start a free review—and we’ll work directly with your attorney to confirm case details and explain your options based on the rules that apply to your lawsuit.

Legal Citations: State Statutes (Full Reference List)

State statutes referenced in this guide (for readers who want the source text).

- Arkansas: Act 915

- California: AB 931 (California Consumer Legal Funding Act)

- Georgia: SB 69

- Illinois: SB 1099

- Indiana: Public Law 153

- Maine: Me. Rev. Stat. tit. 9-A, art. 12 (Legal Funding Practices)

- Missouri: SB 103

- Montana: SB 269

- Nebraska: Neb. Rev. Stat. § 25-3301

- Nevada: SB 432

- New York: A804C / S1104

- Ohio: Ohio Rev. Code § 1349.55

- Oklahoma: Okla. Stat. tit. 14A, § 3-701

- Tennessee: Tenn. Code Ann. § 47-51-101 et seq.

- Utah: HB 312 (Maintenance Funding Practices Act)

- Vermont: Act 128

- West Virginia: SB 360

- Wisconsin: AB 73